Hi, I’m Kushal from India.

When I first started learning about saving and investing, I kept hearing two terms everywhere: Recurring Deposit (RD) and Fixed Deposit (FD). At first, I honestly thought they were almost the same thing because both involved banks, interest rates, and guaranteed returns.

However, after spending some time understanding them, I realized that RD and FD are designed for completely different types of people and financial goals.

One is ideal for people who want to save money gradually every month, while the other works better for people who already have a lump sum amount ready to invest.

If you’re confused between RD and FD, don’t worry. By the end of this guide, you’ll know exactly which one might suit your situation better.

Why Do Beginners Get Confused Between RD and FD?

The confusion is understandable because both products share many similarities.

Both are:

- Offered by banks and financial institutions.

- Considered relatively low-risk options.

- Designed to help grow savings.

- Based on earning interest over time.

Because of these similarities, many beginners assume there is no difference between them.

But the way you invest money in each one is completely different.

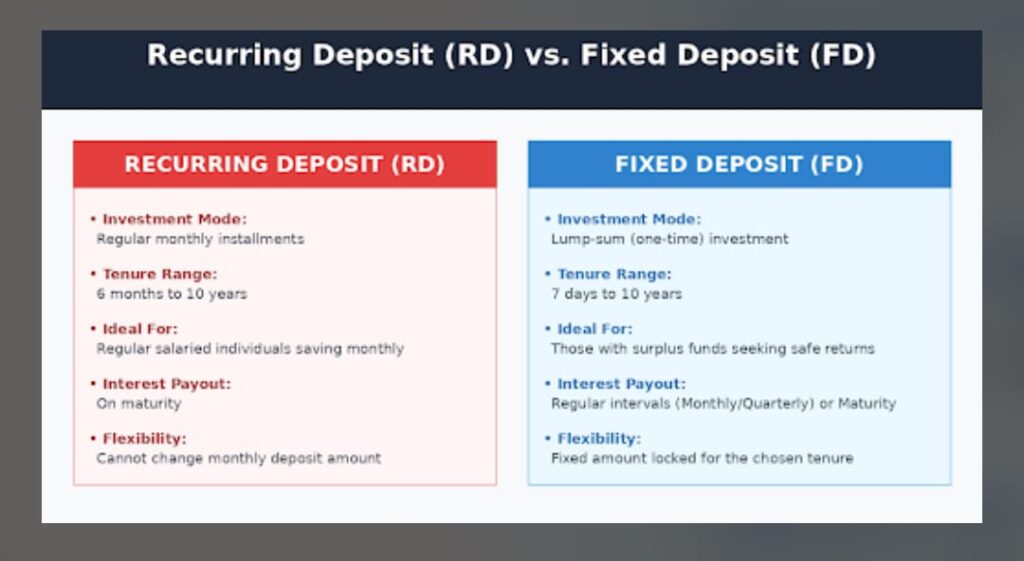

What Is an RD?

RD stands for Recurring Deposit.

In an RD, you deposit a fixed amount of money every month for a chosen period.

Think of it like a monthly savings commitment.

For example:

- $20 every month

- $40 every month

- $50 every month

The bank pays interest on your deposits, and at maturity, you receive your total deposits along with the interest earned.

What Is an FD?

FD stands for Fixed Deposit.

Unlike an RD, you invest the entire amount at once.

For example:

- $500 in one payment

- $1,000 in one payment

- $5,000 in one payment

The money stays invested for a fixed period, and the bank pays interest on it until maturity.

The Simplest Way to Understand the Difference

If I had to explain RD and FD in one sentence, I would say:

RD = Save Monthly

FD = Invest Once

This single line helped me understand the difference when I was learning about banking products.

My Experience While Learning About RD and FD

When I first started saving money, I didn’t have enough savings to open a large FD.

Because of this, I thought investing wasn’t possible for me.

Later, I discovered RDs and realized that even small monthly contributions can help build wealth over time.

A few years later, when I had accumulated some savings, I understood why many people choose FDs for money they don’t need immediately.

This taught me that neither option is better than the other.

The right choice depends on your financial situation.

How RD Works

Let’s take a simple example.

Suppose you decide to invest $30 every month into an RD for 3 years.

Every month:

$30 → Bank Account

After three years, you’ll have deposited a significant amount, and you’ll also receive interest earned during that period.

The biggest advantage is that you don’t need a large amount to get started.

How FD Works

Now imagine you already have $1000 sitting in your savings account.

Instead of leaving it there, you decide to place it into an FD for 5 years.

The bank locks the money for the chosen period and pays interest on the entire amount.

At maturity, you receive:

- Original amount

- Interest earned

This makes FDs attractive for people with existing savings.

Major Differences Between RD and FD

- Investment Method

RD

You invest money every month.

FD

You invest the full amount at once. - Suitable For

RD

People with regular monthly income.

FD

People who already have lump sum savings. - Saving Habit

RD

Helps develop financial discipline.

FD

Does not require monthly contributions. - Flexibility

RD

Suitable for gradual savings goals.

FD

Suitable for parking idle money safely. - Initial Investment Requirement

RD

Can often start with relatively small amounts.

FD

Usually requires a larger initial investment.

Real-Life Example

Let’s imagine two friends.

Priya

Priya recently started her first job.

She wants to save money for higher education after three years but cannot invest a large amount immediately.

She chooses an RD and deposits ₹$30 every month.

Rahul

Rahul recently received a bonus from work.

He already has $2,000 available and doesn’t need the money immediately.

He chooses an FD to earn interest on the amount.

Both made good decisions because they selected products that matched their financial situations.

This is one of the biggest lessons I learned about personal finance:

The best financial product is the one that matches your needs.

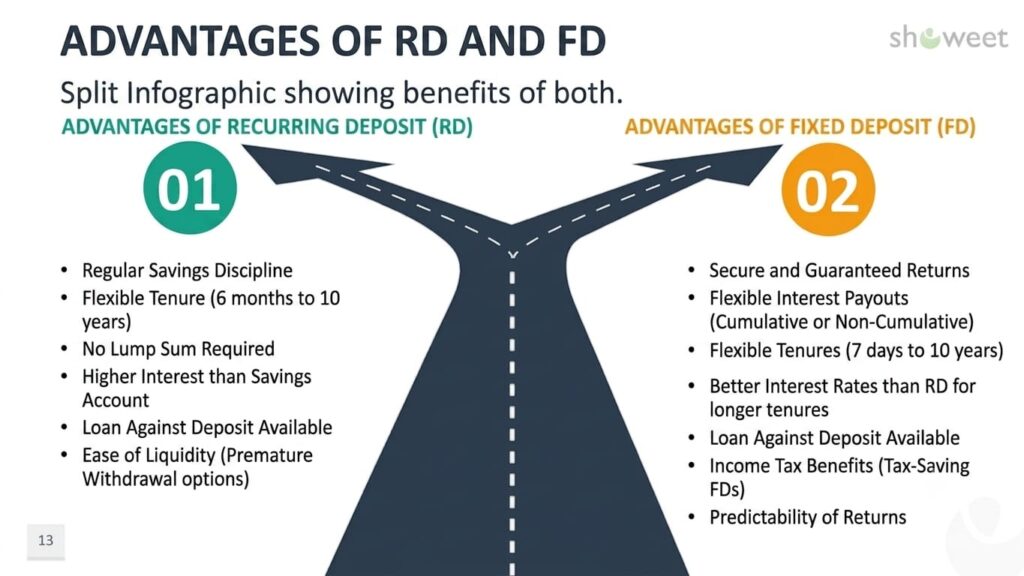

Advantages of RD

Builds Saving Discipline

Regular monthly deposits create healthy financial habits.

Beginner Friendly

Perfect for first-time savers.

Affordable

You don’t need a large amount to begin.

Goal-Based Saving

Useful for vacations, gadgets, education, or future purchases.

Advantages of FD

Guaranteed Returns

You know approximately what you’ll receive at maturity.

Simple and Easy

No monthly deposits to remember.

Ideal for Large Savings

Useful when you already have extra money available.

Stable Investment Option

Many people prefer FDs because of their predictable returns.

Disadvantages of RD

RDs also have some limitations.

- Missing monthly deposits may cause inconvenience.

- Building a large amount takes time.

- Returns may be lower than some investments.

Disadvantages of FD

FDs also have drawbacks.

- Requires a lump sum amount.

- Money may remain locked for a long period.

- Early withdrawals may reduce returns.

Which Is Better for Students?

In my opinion, RDs are often more suitable for students because students usually don’t have large savings available.

Saving a small amount every month is often easier than investing a large amount all at once.

Which Is Better for Salaried Employees?

This depends on the situation.

If you want to save monthly from your salary, an RD can work well.

If you receive bonuses or large payments, an FD may be useful.

Many people actually use both.

Can You Have Both RD and FD?

Absolutely.

This is something I learned much later.

Many people use:

- RD for monthly savings goals.

- FD for protecting lump sum savings.

Using both together can create a balanced savings strategy.

Common Mistakes Beginners Make

In my opinion, these are some of the most common mistakes:

- Choosing FD without having emergency savings.

- Starting an RD with an unrealistic monthly amount.

- Breaking deposits too early.

- Choosing products without understanding their purpose.

- Copying other people’s financial decisions.

Remember, personal finance is personal.

What works for one person may not work for another.

So, Which One Should You Choose in 2026?

Choose an RD if:

- You earn monthly income.

- You want to build saving habits.

- You don’t have a large amount available.

- You’re saving for future goals gradually.

Choose an FD if:

- You already have a lump sum amount.

- You want predictable returns.

- You don’t need immediate access to the money.

- You prefer simple investments.

Final Thoughts

When I first started learning about RD and FD, I spent a lot of time trying to figure out which one was better.

Eventually, I realized I was asking the wrong question.

The better question is:

“Which one fits my financial situation right now?”

An RD helps you build savings slowly and consistently.

An FD helps you grow money that you already have.

Neither option is universally better.

For beginners in 2026, understanding this simple difference can help you make smarter financial decisions and avoid unnecessary confusion.