Hi, I’m Kushal from India.

A few years ago, if someone had asked me where my money went every month, I probably wouldn’t have had a clear answer. I knew how much I earned, but by the end of the month, there always seemed to be less money left than I expected.

Sometimes it was food deliveries, sometimes online shopping, and sometimes small expenses that didn’t seem important at the time. Individually they looked harmless, but together they quietly ate a large part of my monthly income.

That’s when I learned an important lesson:

Most people don’t have an income problem. They have a money management problem.

The solution wasn’t earning more immediately. The solution was creating a monthly budget.

If the word “budget” sounds boring or complicated, don’t worry. A budget is simply a plan for your money before you spend it.

Let’s understand how beginners can create a monthly budget in 2026.

What Is a Monthly Budget?

A monthly budget is a plan that tells your money where it should go every month.

Instead of wondering at the end of the month where your salary disappeared, you decide in advance how much money will be used for:

- Rent

- Food

- Savings

- Bills

- Transportation

- Entertainment

- Investments

In simple words:

A budget gives every rupee a job.

Why Is Budgeting Important?

Many people avoid budgeting because they think it will limit their freedom.

Ironically, the opposite is often true.

When you know exactly where your money is going, you usually feel more in control and less stressed.

- A good budget can help you:

- Avoid unnecessary spending.

- Build savings faster.

- Prepare for emergencies.

- Reach financial goals.

- Reduce money-related stress.

My Experience With Budgeting

When I first tried budgeting, I made a common mistake.

I created an extremely strict budget that allowed almost no room for fun spending.

Within two weeks I completely ignored it.

Later I realized that a good budget should work with your lifestyle, not against it.

Budgeting isn’t about removing enjoyment from life.

It’s about making sure your spending matches your priorities.

That simple mindset change made budgeting much easier for me.

Step 1: Calculate Your Monthly Income

The first step is understanding how much money comes in every month.

For example:

- Salary

- Freelance income

- Business income

- Rental income

- Side hustle income

Let’s assume your total monthly income is:

$800

This becomes the starting point of your budget.

Step 2: Track Your Expenses

This step surprises many beginners.

Most people underestimate how much they spend.

Write down every expense for one month.

Examples include:

- Rent

- Electricity

- Internet

- Mobile recharge

- Fuel

- Groceries

- Subscriptions

- Online shopping

- Dining out

Even small expenses matter.

That $1.5 coffee or $3 food delivery may not seem important individually, but repeated purchases add up quickly.

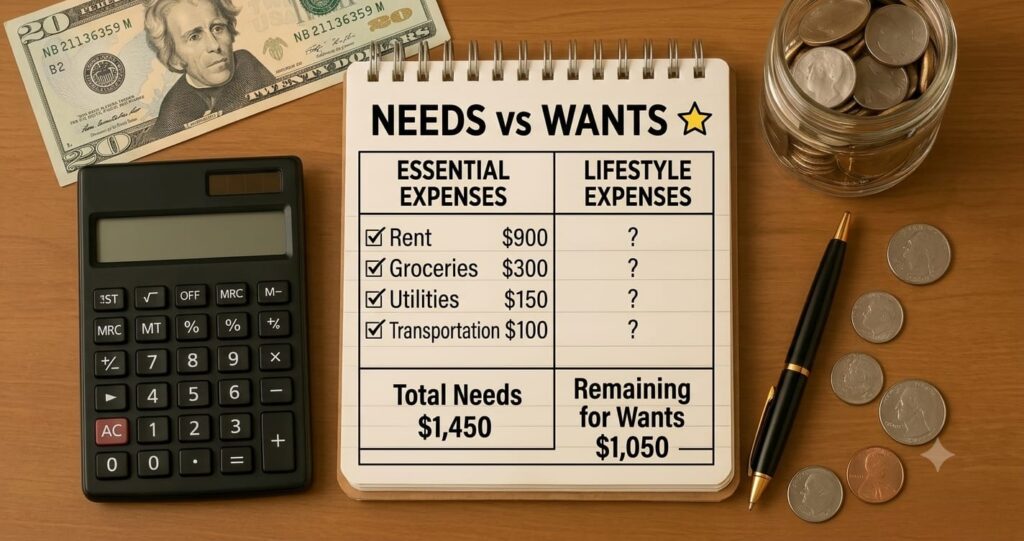

Step 3: Separate Needs and Wants

This is one of the most useful budgeting exercises.

Needs

These are expenses required for daily life.

Examples:

- Rent

- Groceries

- Utilities

- Transportation

- Insurance

Wants

These are optional expenses.

Examples:

- Streaming subscriptions

- Gaming purchases

- Expensive dining

- Luxury shopping

Understanding this difference helps improve spending decisions.

Step 4: Pay Yourself First

This was one of the best financial lessons I ever learned.

Most people save whatever money remains at the end of the month.

Unfortunately, very little usually remains.

Instead:

Save first.

Spend later.

For example:

Salary Received → Savings → Expenses

Even saving 10% of your income consistently can make a huge difference over time.

Step 5: Create Spending Categories

A simple example budget for $800 monthly income might look like this:

Category Amount

Housing $150

Food $80

Transportation $40

Savings $70

Investments $50

Entertainment $30

Miscellaneous $80

The numbers will be different for everyone.

The goal is not perfection.

The goal is awareness.

Step 6: Build an Emergency Fund

Unexpected expenses happen.

- Medical bills

- Vehicle repairs

- Job loss

- Family emergencies

Without emergency savings, people often rely on debt.

Even small monthly contributions toward an emergency fund can create financial security.

Step 7: Review Your Budget Monthly

Your budget should evolve as your life changes.

A budget that worked last year may not work today.

Review your spending regularly and make adjustments when necessary.

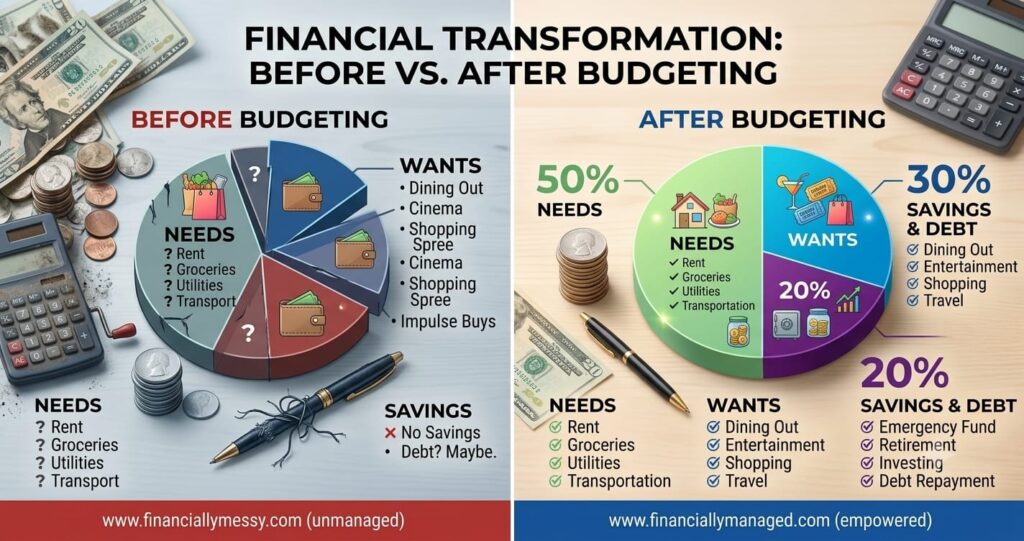

The 50/30/20 Rule

One popular budgeting method is the 50/30/20 rule.

50% for Needs

Housing, food, bills, transportation.

30% for Wants

Entertainment, hobbies, shopping.

20% for Savings and Investments

Emergency fund, retirement, investing.

This method isn’t perfect for everyone, but it provides a useful starting point for beginners.

Real-Life Example

Let’s imagine Priya earns $700 per month.

Before budgeting:

- Frequent online shopping

- Food delivery several times a week

- Very little savings

After creating a budget:

- Spending became more intentional.

- Savings increased.

- Financial stress reduced.

Interestingly, her income didn’t change.

Only her financial habits changed.

Common Budgeting Mistakes

In my opinion, these are some of the biggest mistakes beginners make.

Creating Unrealistic Budgets

Budgets that are too strict rarely last.

Forgetting Annual Expenses

Insurance payments and festivals still need planning.

Ignoring Small Purchases

Small expenses can become surprisingly large over time.

Not Reviewing the Budget

Budgets need updates.

Trying to Be Perfect

Progress matters more than perfection.

Budgeting Apps vs Traditional Methods

Some people prefer:

- Mobile apps

- Banking apps

- Spreadsheets

Others prefer:

- Pen and paper

- Notebooks

- Physical planners

There is no right answer.

The best budgeting system is the one you actually use consistently.

How Budgeting Changes Your Mindset

One unexpected benefit of budgeting is that it changes the way you think about money.

Instead of asking:

“Can I afford this today?”

You begin asking:

“Does this purchase support my financial goals?”

That small shift can completely change spending behavior.

Is Budgeting Only for People With Low Income?

Absolutely not.

People at every income level can benefit from budgeting.

In fact, high-income earners often face financial problems because higher income does not automatically guarantee better money management.

Financial discipline matters more than income alone.

Final Thoughts

When I first started learning about personal finance, budgeting felt restrictive and unnecessary.

Today, I see it differently.

A budget isn’t a punishment.

It’s a financial roadmap

It helps you spend with confidence, save with purpose, and prepare for the future.

For beginners in 2026, creating a monthly budget may be one of the most valuable financial habits you ever build.

Because at the end of the day, financial success isn’t only about how much money you make.

It’s also about how well you manage the money you already have.

Great content! Keep up the good work!

Thanks