Hey I am Kushal from India. When I first heard the term “Personal Loan” I thought it was something only people with financial problems used. But after learning more about it, I realized that a personal loan can actually be a useful financial tool when used responsibly.

In this beginner-friendly guide, I will explain everything you need to know about personal loans in simple language.

What Is a Personal Loan ?

A Personal Loan is a type of loan that allows you to borrow money from a bank or financial institution and repay it over a fixed period through monthly installments.

A personal loan is different to a home loan or car loan because the money is not always needed for a specific purpose, so you are not required to provide details of the intended use of funds. This allows for more flexible borrowing.

Example:- if you need money for medical treatment, education expenses, travel, home renovation, or a family event, you may use a personal loan for those purposes.

Why Do People Take Personal Loans ?

Everyone’s financial situation is different. Sometimes unexpected expenses appear when we are not financially prepared.

Here are some common reasons people take personal loans :

Medical Emergencies

Unexpected hospital bills can be expensive. A personal loan can help cover urgent medical costs.

Home Renovation

Many people use personal loans to repair or improve their homes.

Wedding Expenses

Weddings can be expensive and many families take on personal loans.

Education Costs

Students or parents on behalf of students, may obtain a personal loan for educational expenses.

Debt Consolidation

Some people use personal loans to combine multiple debts into a single monthly payment.

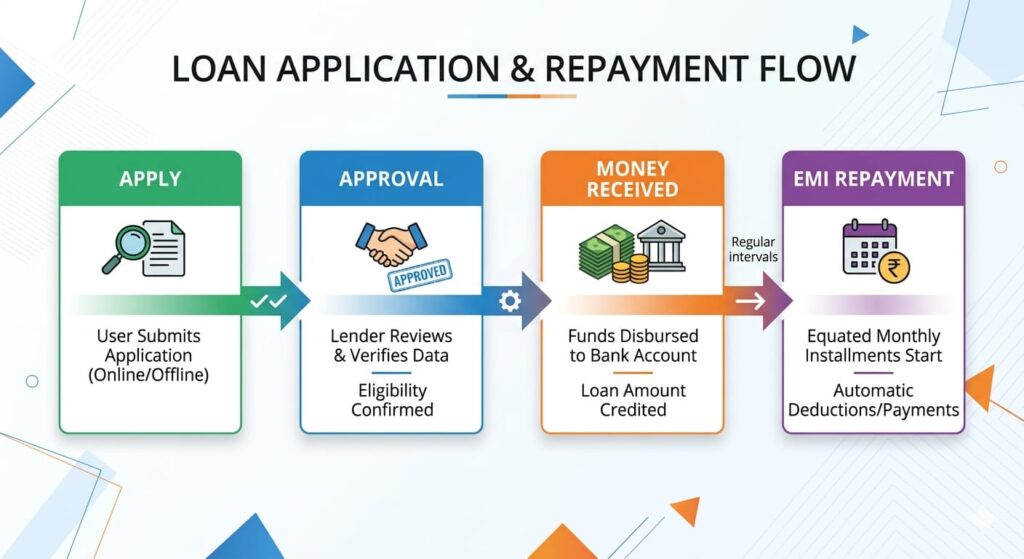

How Does a Personal Loan Work ?

A personal loan works in a simple way.

First you borrow money for the property from a bank or lender. If the bank agrees to lend you the money, you borrow it.

After you borrow the money, you then pay it back to the bank in the form of EMIs (Monthly installment paid to the bank) for a specified period.

Each EMI usually includes :

- A portion of the borrowed amount

- Interest charged by the lender

The repayment period can range from a few months to several years, depending on the lender and loan amount.

Understanding Interest Rate

One of the most important things to understand before taking a personal loan is the interest rate.

The interest rate is the extra amount you pay for borrowing money.

For example:- if you borrow $10,000, you will repay more than $10,000 because the lender charges interest.

Different lenders offer different interest rates based on factors such as :

- Credit score

- Income

- Employment status

- Loan amount

- Repayment history

A lower interest rate means lower overall borrowing costs.

Benefits of a Personal Loan

Personal loans offer several benefits.

Quick Access to Funds

Many lenders process personal loans quickly, especially for eligible applicants.

No Collateral Required

Most personal loans are unsecured, meaning you usually do not need to pledge property, gold or other assets.

Flexible Usage

You can use the money for many personal purposes.

Fixed Repayment Schedule

Monthly payments are generally fixed, making budgeting easier.

Helpful During Emergencies

A personal loan can provide financial support when immediate funds are needed.

Disadvantages of a Personal Loan

A lot of people consider personal loans to be helpful, but they do have their disadvantages.

Interest Costs

Personal loans generally have higher interest rates compared to secured loans.

Monthly Financial Commitment

You have to keep up the repayments each month even if you are experiencing financial hardship.

Risk of Debt

Taking out too much of a loan can cause problems.

Additional Charges

Some lenders can impose processing charges, late payment fees and other costs.

Who Should Consider a Personal Loan ?

A personal loan may be suitable for people who :

- Have a genuine financial need

- Can comfortably repay monthly installments

- Need quick access to funds

- Do not have enough savings for a major expense

However, it is generally not a good idea to take a loan for non-essential shopping or luxury items.

Common Mistakes Beginners

In my opinion, one of the biggest mistakes beginners make is focusing only on the loan amount and ignoring the total repayment cost.

Some common mistakes include :

- Borrowing more than needed

- Not comparing lenders

- Ignoring interest rates

- Missing EMI payments

- Taking loans for unnecessary expenses

These mistakes can increase financial pressure and make repayment difficult.

Things to Check Before Taking a Personal Loan

Before applying for a personal loan, ask yourself a few questions :

Do I Really Need This Loan ?

Sometimes saving money may be a better option than borrowing.

Can I Afford the EMI ?

Your monthly payments should comfortably fit within your budget.

Have I Compared Multiple Lenders ?

Comparing offers may help you find lower interest rates and better terms.

Do I Understand All Charges ?

Always read the loan agreement carefully.

A Simple Real Life Perspective

While learning about personal loans, I realized that many people use them when they need money urgently and their savings are not enough. A personal loan can be helpful in such situations, but it should always be used responsibly because the borrowed money must be repaid with interest.

Conclusion

Personal loans are one of the more flexible means of borrowing and can be very helpful for people needing to pay for essential items when they have inadequate savings available. They provide quick funds and are of value in times of need.

However, a personal loan should always be used responsibly. Before borrowing money, understand the interest rates, repayment terms, and your ability to make monthly payments. Making informed decisions can help you avoid unnecessary debt and maintain better financial health.

Keep in mind that a loan can be a quick fix to a short-term money issue, but it’s the repayment that stands to safeguard your financial health.

BY- KUSHAL